The Judgment Premium: Why the $1T Opportunity Is in Selling Work, Not Software

Discover why the next trillion-dollar AI shift isn't about better SaaS tools, but "Autopilots" that sell completed work. My take on Sequoia Capital's latest thesis on the $1T services market.

When I first read Sequoia’s latest thesis, “Services: The New Software,” I was skeptical. Another prediction about AI replacing jobs? But as I read, I realized this was different. The viewpoint they present isn’t just about automation; it’s a fundamental shift in how we value human capability.

The core premise is undeniable: the next trillion-dollar company won’t be a SaaS giant selling you a better dashboard. It will be a software company masquerading as a services firm, selling you the completed work itself.

“A company might spend $10K a year for QuickBooks and $120K on an accountant to close the books. The next legendary company will just close the books.” [1]

This shift from selling tools (Copilots) to selling outcomes (Autopilots) is going to rewrite the rules for every agency, consultancy, and professional services firm on earth. Here is why this matters, and how it changes the game for builders and buyers alike.

Check out my previous articles and subscribe to keep yourself updated with the latest happenings.

The Intelligence vs. Judgment Divide

The most profound insight from the report is the distinction between intelligence and judgment.

“Writing code is mostly intelligence. Knowing what to build next is judgement. Translating a spec into code, testing, debugging: the rules are complex but they are rules. Judgement is different. It requires experience and taste, instinct built on years of practice. Deciding which feature to build next, whether to take on tech debt, when to ship before it’s ready.” [1]

Writing code, translating a spec, testing, and debugging - these are acts of intelligence. The rules are complex, but they are still rules. AI is exceptionally good at learning rules.

Judgment is entirely different. Judgment is deciding which feature to build next. It’s knowing when to take on technical debt to hit a market window, or having the taste to know when a product is ready to ship. Judgment is instinct built on years of practice.

As AI commoditizes intelligence (the how), the market value is rapidly shifting to judgment (the what and why). Sequoia puts it plainly: “Today’s judgement will become tomorrow’s intelligence.” [1]

This creates a fascinating paradox for the workforce. If AI handles the “grunt work” of intelligence, how do junior professionals ever develop the experience required for high-level judgment?

We are entering an era where companies will place a massive premium on seasoned professionals who possess this taste. However, freshers still hold a unique advantage: they approach problems from first principles, unburdened by “how it’s always been done,” allowing them to innovate in ways experienced veterans might miss entirely.

Copilots vs. Autopilots: The Architecture Shift

The transition from intelligence to judgment is driving a massive shift in product architecture.

“A copilot sells the tool. An autopilot sells the work.” [1]

Until recently, AI models were still developing intelligence and judgment, so the right approach was to build a copilot first: put AI in the hands of a professional and let them decide what to do with it. Companies like Harvey sell to law firms, and Rogo sells to investment banks. The professional is the customer, the tool makes them more productive, and they take responsibility for the output.

Today, the models are intelligent enough that in some categories the best place to start is as an autopilot. Crosby sells to the company that needs an NDA drafted, not to outside counsel. WithCoverage sells to the CFO who needs insurance, not to the broker. The customer is buying the outcome directly.

The higher the intelligence ratio in any field, the sooner autopilots will win.

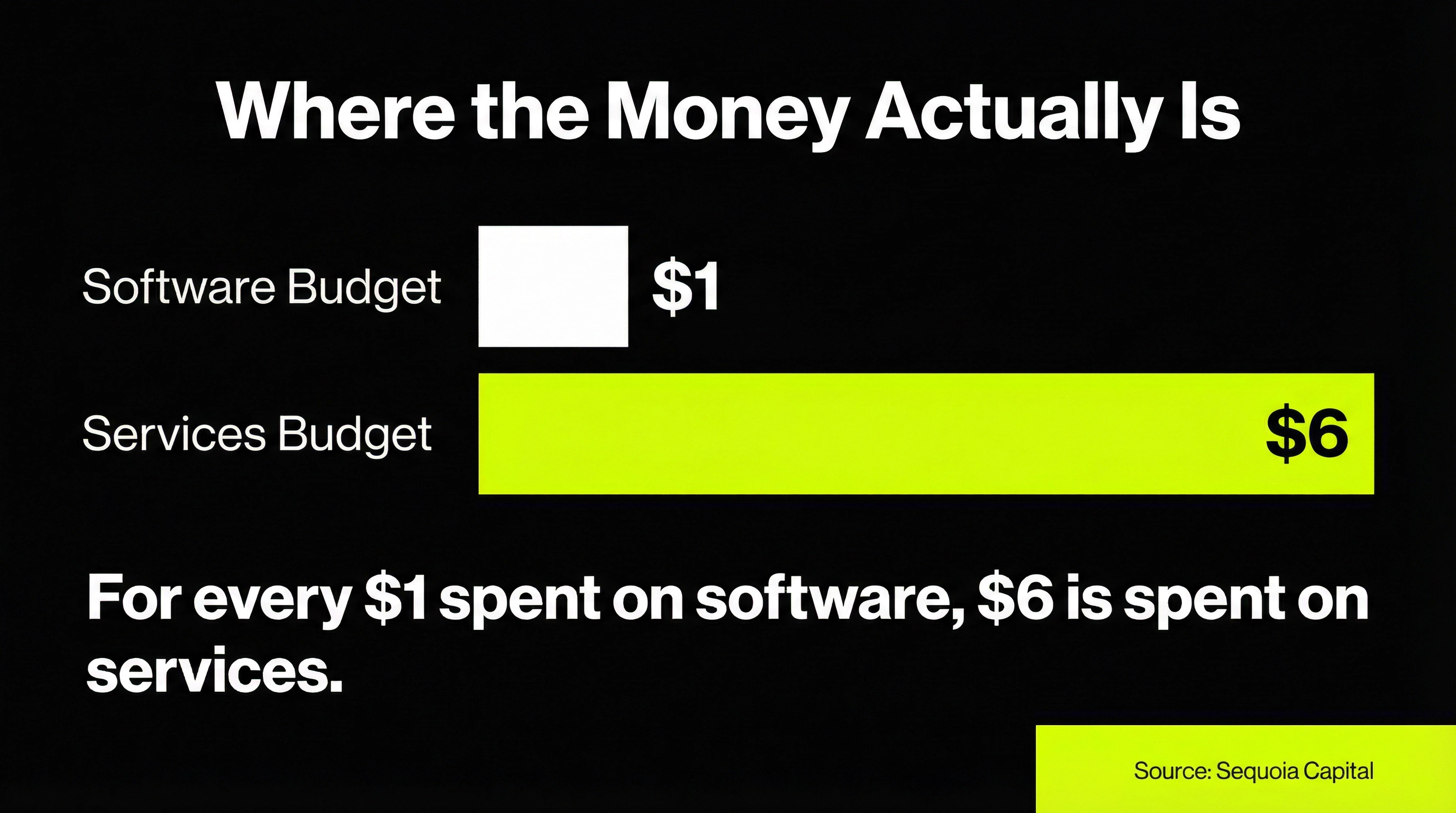

The 6:1 Ratio: Why Services Are the Real Prize

If you want to understand why AI companies are pivoting to services, look at the math.

The work budget in any profession dwarfs the tool budget. Traditional SaaS companies fight viciously over that single software dollar. AI-native service providers (Autopilots) are bypassing that fight entirely and capturing the six-dollar work budget from day one.

The customer doesn’t want to buy a tool and learn how to use it; they want to buy the outcome directly.

This is the fundamental reason why the next $1T company won’t be a SaaS platform - it will be an AI-native services firm.

The Outsourcing Wedge: Vendor Swaps vs. Reorgs

So, where does this revolution start? It starts with outsourced work.

The playbook is clear: companies should start with the outsourced, intelligence-heavy task. Nail distribution. Expand toward the insourced, judgment-heavy work as the AI compounds. The outsourced task is the wedge. The insourced work is the long-term TAM.

Crosby started with NDAs: a well-defined task, primarily intelligence, that most companies already outsource to external counsel. The budget exists, the scope is clear, the ROI is immediate, and the substitution is frictionless. [1]

This is why the initial wave of AI disruption isn’t targeting internal teams; it’s targeting the BPOs, the external agencies, and the managed service providers.

The Opportunity Map: Where Autopilots Are Winning Now

Sequoia maps out the massive TAM across various service verticals. Here is a look at where the autopilot revolution is already taking hold:

Source: Sequoia Capital, “Services: The New Software” (2026)

The agent deployment picture is equally revealing:

Source: Sequoia Capital, “Services: The New Software” (2026)

Software engineering got to autopilot first because it’s primarily intelligence work. Every other profession is following the same path, just a few years behind.

The Boutique Revolution: Small Teams, Massive Output

What does this mean for the future of the services sector? We are about to witness the rise of the “Boutique Agency” on steroids.

The traditional model relied on massive headcount to scale revenue. Giants like Accenture or TCS built empires on this premise. But in the AI-native era, team size is no longer correlated with output.

A 10-person specialised agency, armed with the right AI agents, can now deliver the volume and quality of a 500-person firm. The team size shrinks, but the capacity to deliver massive projects expands. Unless the legacy giants radically change how they operate, these hyper-efficient boutique firms will start winning their contracts.

This is also correlated with the wave of layoffs we’ve seen at large IT services companies. It isn’t just a market correction - it’s a structural shift. The companies that adapt fastest will survive. The ones that don’t will find their margins eroded by 10-person startups operating at 10x their efficiency.

The Rise of the Architect-PM

This shift also redefines the most valuable roles in tech. For the first time, we might need more Product Managers than traditional Software Engineers.

If AI is writing the code, the “Engineering” role evolves. The new elite builder is an “Architect-PM” - someone who possesses the technical IQ to architect complex systems, combined with the deep user empathy required to solve real human pain points. They aren’t just translating specs into code; they are solutioning what the user actually needs.

The best professionals in the next decade won’t be the ones who can write the most code. They will be the ones who can ask the right questions, understand the user’s pain at a deep level, and architect a system that solves it elegantly.

Who Wins, Who Gets Disrupted

The services sector is about to be split into two camps:

Winners: AI-native autopilot companies in high-intelligence verticals (insurance, accounting, legal, healthcare billing, IT support). Boutique agencies with deep domain expertise and AI fluency. Senior professionals with strong judgment and taste. Freshers who embrace first-principles thinking over conventional wisdom.

Under Pressure: Large BPOs and IT services firms that rely on headcount arbitrage. Mid-level professionals in purely intelligence-heavy roles (basic coding, data entry, form processing, standard contract drafting). Traditional SaaS tools that sell to professionals rather than directly to outcome-buyers.

The Verdict

Sequoia’s thesis is a wake-up call. The era of selling software as a tool is peaking. The era of selling software as a service - literally doing the work - is just beginning.

Whether you are building an AI startup or running a services firm, the mandate is clear: stop selling the hammer, and start selling the house.

The companies that understand this shift early will capture the six-dollar budget. The ones that don’t will keep fighting over the one-dollar budget - and wonder why growth is slowing.

References

[1] Sequoia Capital. “Services: The New Software” by Julien Bek. Published March 5, 2026. https://sequoiacap.com/article/services-the-new-software/